Want to know the power of cashflow? Why am I living paycheck to paycheck? How do the rich get richer?

Cashflow

Ever wonder how the rich get richer? Ask yourself why am I living paycheck to paycheck? How it possible to invest when I don’t have money?

What is Cashflow?

What is cashflow???

Money coming in – money going out = (+/-) cashflow

Cashflow can be calculated many ways. The way I calculate cashflow is per month.

I take all streams of income and add it all together (if you only have one, that’s totally fine).

Then, add up all your debt. Things that require a monthly payment (for example: cell phone bill, car bill, insurance, rent, utilities and food, etc.)

I like to be conservative when calculating things that can change from month to month, for example food/ dining.

You may dine out a few times a month, normally. The next month you may dine out an extra night so add a little extra to dining when calculating.

Read to the end and get my “Cashflow Spreadsheet” totally FREE!

The power of cashflow!!!

Cash flow is the foundation of any wealth building strategy. The opposite of cashflow is Debt!

Cashflow is like a river. The water resembling money and everything in and around that river resembles life (it was the best analogy that resembles cashflow).

You can increase the flow of water or you can decrease the flow of water. Without water, every living thing that depends on that river will die! Animals, plants, insects then of course humans!

Cashflow can be affected in many ways very much like a river can lose its flow: loss of a job, changing jobs, becoming incapacitated, large purchases, tons of small unnecessary purchases!

There are so many ways that can dramatically affect your cashflow quickly without even noticing it.

Take one simple thing we do every day. For example, food we like to eat?

Or maybe even a coffee that we get from our favorite coffee shop? Think about how much we spend each time we go there.

How many times a week do we go there?

Then how many times in a month do we go there? I think you’re getting the point. Let’s combine this with some numbers to make it more interesting…

My favorite drink from Starbucks is the Iced, Venti, Soy, stirred, caramel macchiato (yes, that’s one drink, lol) it costs about $4.75 without tax.

Let’s round up to $5.00 to make this simple. I used to go there every day before I headed into work which was 4 days a week ($20).

Then that would be a total of 16 days a month ($80).

Let’s take it further and multiply that by 12 months ($960). Whaaaaaat??? Yup, almost $1,000 on a single drink! See how fast that adds up?

Let’s continue with the river analogy… Let’s say that there is a landslide and the debris are blocking a section of your river. What will happen? Your river will begin to back up causing less flow to the necessary parts that are downstream.

Remember if flow of river is (cashflow) then when a river is backing up, you’re accumulating, you guessed it! DEBT!

Everything that is downstream will suffer! Like a river, we need that flow of money (water) to pay for bills which occur monthly, food which is daily and debt (good or bad).

If the water makes it to the end and successfully nourishes all living things, then that is when you have a steady flow of money you have a savings or a grow bed what I like to call it (love to garden so I love this analogy). As you bear fruit or veggies is when you know your plants are nourished and receiving the necessary nutrients.

What is Bad Debt?

What causes a backup in your river?… Bad DEBT!

Debt can cause major backups! But let’s not get good debt and bad debt mixed up!

The debt I’m referring to is credit card debt, personal loans, vehicle loans, student loans, gambling debt (in Hawaii it’s a real thing and you don’t want some angry Hawaiian coming to your doorstep for his money).

These types of debts have no return on investment (ROI)… unless of course you took out a personal loan for 20K and invested into TSLA when it was at $100… But that’s another topic which I’ll cover in a later post.

Bad debt can come in all forms but let’s face it, credit cards are too easy to get and too easy to use!

How to effectively use a credit card?

There are a lot of stigmatisms toward credit cards but credit cards can be very useful if you use them the right way.

Everyone should use a credit card, but not to splurge on a new outfit or to purchase new rims for their car or buying everyone at the bar a round of drinks…

although I know a lot of people who do…

Once you have a balance that you’re carrying over from month to month, this can be the number one cashflow killer! (Could arguably be number two with car loans coming in #1)

You should never view your credit card as a loan… ever!

All it takes is one purchase that forces you to carry a balance for months, sometimes even years that could slow the flow if not kill the flow of money coming in for a very long time.

I only use my credit cards for everyday purchases like food, fill my truck up with gas, I even use it to pay for my cell phone bill month to month but this will depend on your credit line and your budget.

Every month it is important to pay off your entire balance every single month! I can’t stress how important it is to do this. Once you carry over a balance, then this where the interest rate on a credit card can hurt you (financially of course not physically).

You could have a credit card with a %1,000,000,000 interest rate and if you don’t carry a balance then that interest rate is irrelevant.

If you use a credit card properly, you could dramatically increase your credit score and you can get cash back of miles if you’re an enjoy traveling and use a specific airline.

Loans

Car loans…

I see this WAAAY too often… but do really need a car that costs forty thousand dollars??? Of course not!

Spend within your means is such a critical “saying” to obey!

What you do need is a reliable and efficient means of transportation to and from work, nothing more!

This doesn’t always have to be a car or truck! It could be a bicycle, skateboard, scooter anything that makes sense for your specific situation and that fits your budget.

Let’s be honest, catching public transportation isn’t fun and can cost you time, TIME IS MONEY! I mean unless you live in the city and it makes sense for your personal situation.

A skateboard or bicycle wouldn’t make sense if you work 20+ miles away.

What about a motorized scooter or motorcycle? Low on gas and probable cheaper than owning a car but can still efficiently get you to and from work.

In Hawaii we have public transit that could be a difference of getting to work in 1-1 ½ hours or if you had a vehicle, you’d get to work in 20 minutes! So, in Hawaii it’s critical to have a means of transportation.

If you’re purchasing a vehicle, don’t get caught up with getting something that is flashy to impress people or to simply make yourself “feel good” but instead think about the goal you’re visualizing 5 or maybe 10 years from now. Or simply to increase your CASHFLOW!

It’s hard to see now but years from now when you start to see your grow beds flourishing, then you’ll be able to make these purchases (potentially even paying cash!)

Let’s break this down really quick because it’s very important to understand how this can affect you dramatically.

Say you bought a car/ truck for 40K and did a 6-year loan (I’m being conservative to keep the cost down) that would be about $555/ month (this number is not reflecting the interest on the loan).

Your average monthly (net) income is $3,000 minus $555, you now have $2,445. Your rent is about $1200 which leaves you with $1,245 not including all your utilities: electric, gas, internet, water, sewer, etc.

Ok you have about $1,000 left after all of the above is taken care of… Oh, do you have a cell phone? Take another $100 off now you have $900.

Are you a Starbucks junky? How much food do you consume a week? Take another $20/day x 5 days a week, that leaves you with $500 a month in cashflow. whew!

What if you got a car or personal loan (used car loans can vary, depending on how old the car is because that could be a liability for the bank) for about $5,000 or maybe even $10,000 if you want get somewhat fancy, lol.

Say you took out a 10k loan a 6-year term (not including interest) that would be about $139 a month. Let’s minus the prior example’s monthly loan amount to the current ($555 – $139 = $416 cashflow). Multiply this by 72 months (6 years for the loan) and this will give you $29,952!!! Holy moly!!!

It’s pretty easy to see how a loan, more specifically a car loan, can hurt your cashflow… but hey some things are essential. Transportation to and from work can be a difference of getting to work in 15 minutes or 1 hour (depending on public transportation routes). That time will add up over time, lol if that makes sense.

Car loans, student loans, personal loans and conventional home loans are “amortized” loans. So pretty much what this means is the bank will give you the loan but since they are taking a risk and giving you money for a certain amount of time, they are charging you interest and this will be a “frontloaded” type loan.

A frontloaded means that the interest to principal ratio will be higher in the first half of the loan, which will eventually transition into higher principal once you pass the halfway mark in your term of the loan.

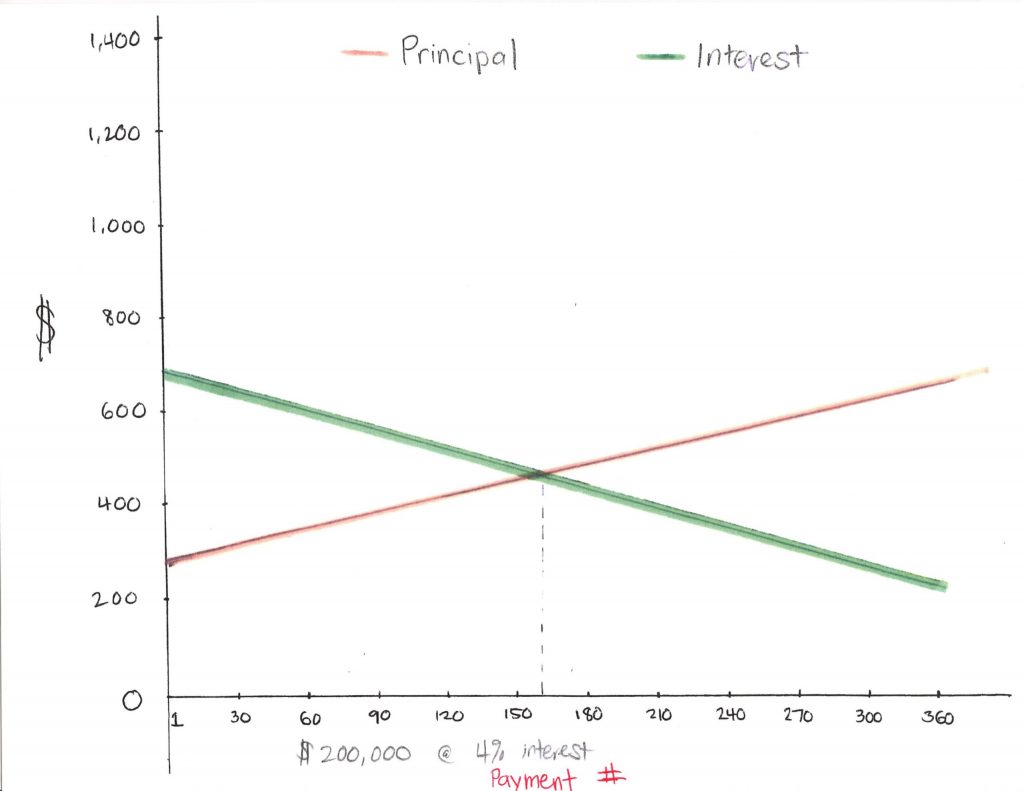

The illustration below (don’t mind my artwork) shows what an “amortized” loan looks like. The vertical (y axis) represents the dollar and the horizontal (x axis) represents payment number throughout the life of the loan (1-360 months or 30 years)

The bottom line is, loans can seem like a harmless thing to acquire but it can suck up your cashflow. Just be practical when deciding on a loan.

Budgeting

Budgets are the summary of what’s happening to your money in and money out monthly. You need to set up a budget to ensure that you’re cashflow positive and not cashflow negative! I’ve set up a simple budget spreadsheet that you can use for FREE! Just plug in your numbers and voila!

The balance on the bottom will tell you if you need to trim your spending in a certain area based on your negative or positive number.

Just remember You can’t trim from your bills so hopefully you’re cashflowing positive!!! If you’re not cashflow positive, a good place to trim back would be under “miscellaneous”.

Side Hustle!

In my opinion everybody should have a side hustle! This is an absolute must! Every single person no matter what your background may be should be considering something they can do on the side to earn extra income.

Preferably, not a second “job” or W-2 but maybe a small business that you own (for tax benefits) or even something like trimming the neighbor’s yard for cash! ANYTHING!

The extra income can come in clutch especially during a month where unforeseen expenses arise. Trust me if you don’t account for the unexpected than you’re failing to plan. I’ve always believed in the saying “FAIL TO PLAN, PLAN TO FAIL!” simple!

So now that you understand the power of cashflow, get out there and get that river flowing!